Pension benefits finallyAvailable to more Canadians

The Family Pension Plan (FPP) was designed and introduced to the Canadian market about four years ago for self-employed professionals that did not have access to the many benefits offered by pension plans. To qualify for the Family Pension Plan (FPP), business owners and incorporated professionals must be between 18 and 71 years old and receiving a T4 income.

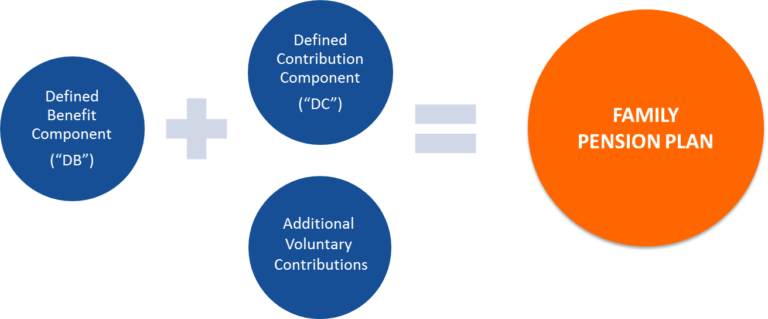

The Family Pension Plan (FPP) allows its members to put the largest amount of money permitted by the Income Tax Act in a tax-deferred vehicle to save for their retirement. For a full list of the benefits allowed within the Family Pension Plan, please contact us.